- Buy Crypto

- Markets

- Futures

- Spot

- Copy Trade

Earn

Earn- More

The old altcoin script is outdated, take you to decipher the new market structure

Original Article Title: The New Market Regime

Original Article Author: David Attermann

Original Article Translation: SpecialistXBT

Editor's Note: Why hasn't the "Altseason" appeared in this cycle? The author points out in this article that the old market paradigm relying on high leverage and speculation has come to an end, replaced by a new regime dominated by regulatory thresholds and institutional capital. In this new framework, investment logic will shift from capturing liquidity overflow to filtering long-term value assets with genuine utility and regulatory adaptability.

Below is the original content:

Since 2022, altcoins' widespread underperformance reflects a shift in the underlying structure rather than a typical market cycle.

The liquidity architecture that once widely transmitted capital to all ends of the risk curve has collapsed and never been rebuilt.

In its place is a new market regime that has altered the way opportunities are generated and captured.

The collapse of Luna in 2022 dismantled the liquidity architecture that used to transmit capital down the cryptocurrency risk curve. The market did not crash suddenly on October 10; it had ruptured years earlier, and everything since then has been aftershocks.

The post-Luna era has seen the most bullish macro, regulatory, and fundamental backdrop in cryptocurrency history. Traditional risk assets and gold have surged, but the long tail assets of the crypto market have not. The reason is structural: the liquidity system that once drove broad asset rotation no longer exists.

This is not the loss of a healthy growth engine. This is the breakdown of a market structure fundamentally mismatched with enduring value creation.

2017-2019:

2020-2022:

May 2022 to Present:

(Note: "OTHERS" = Cryptocurrency total market cap excluding the top ten tokens)

Despite the most favorable macro backdrop, altcoins remain stagnant

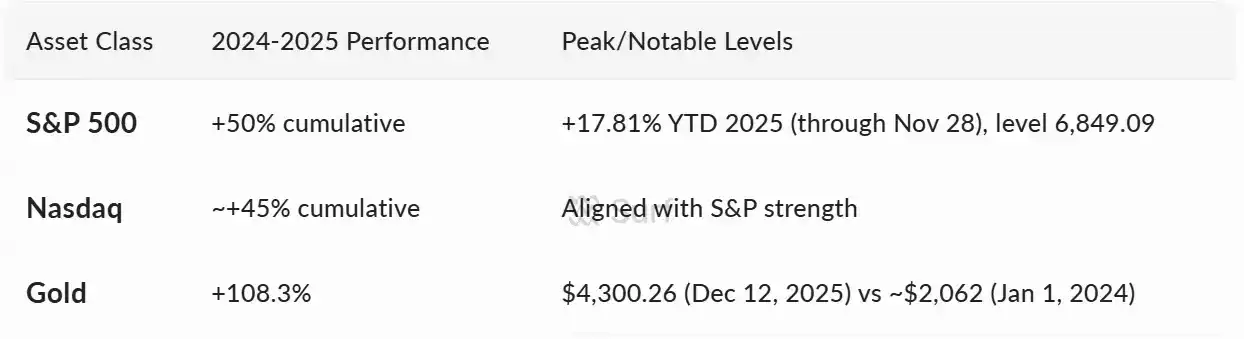

In the years following the Luna collapse, especially in 2024-2025, the crypto industry witnessed an unprecedentedly strong combination of macro environment, regulatory policies, and fundamental bullishness. Under the pre-Luna market structure, these forces would typically reliably trigger deep risk curve rotations. However, what has puzzled crypto investors is that this scenario has not unfolded in the past two years.

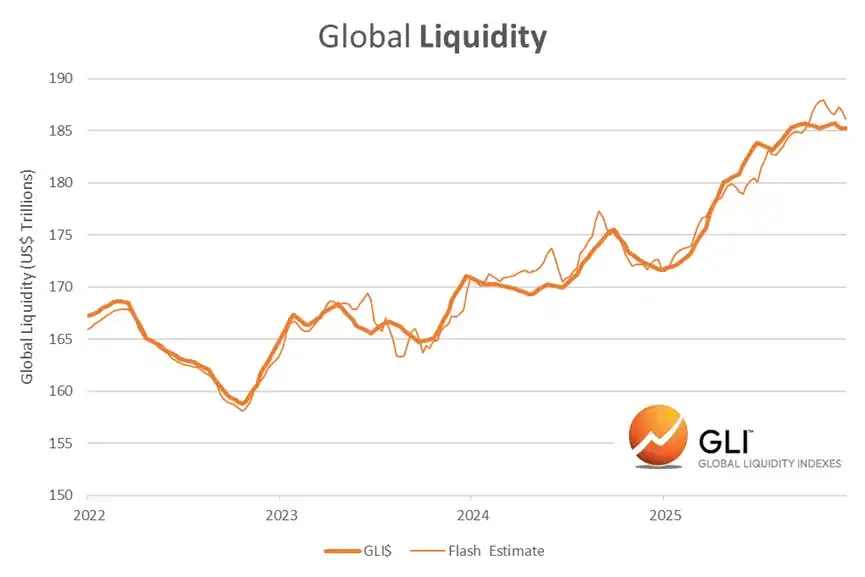

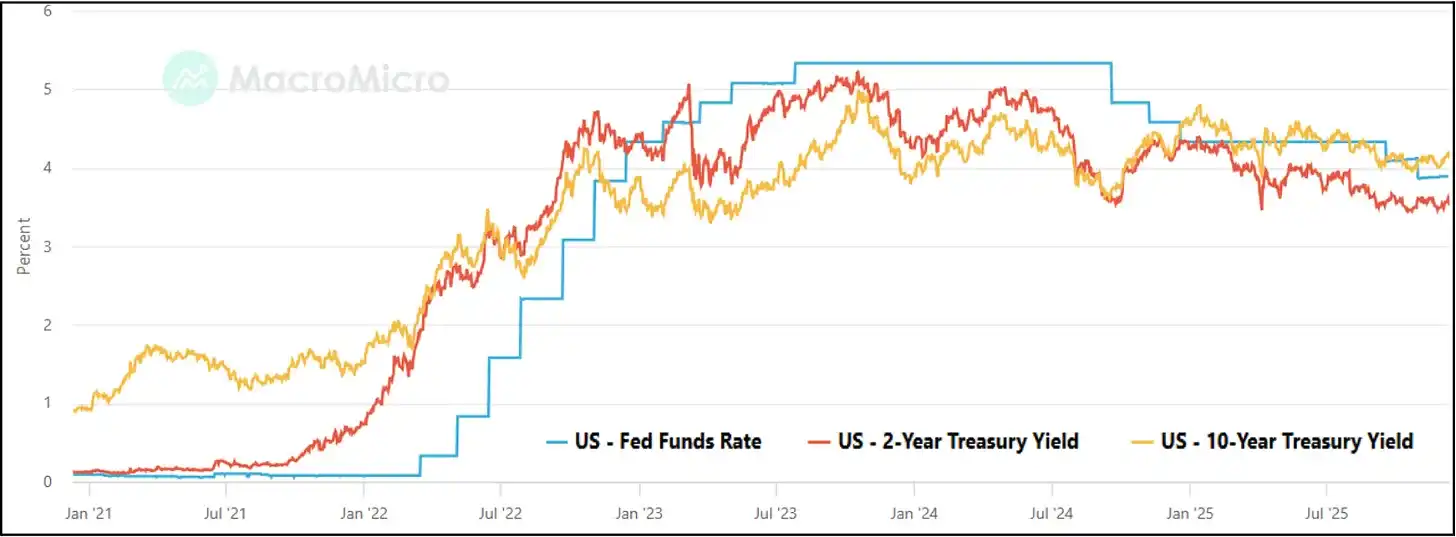

Ideal Liquidity Conditions

Global liquidity expansion, decreasing real interest rates, central banks shifting to a Risk-on mode, traditional risk assets repeatedly hitting new highs.

Strong Regulatory Momentum

· Regulatory clarity process, a long-standing hurdle for large-scale allocators, accelerating:

· US welcomes its first crypto-supportive administration.

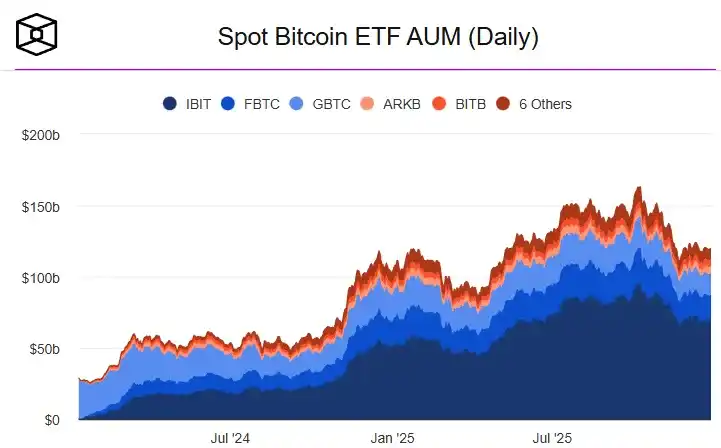

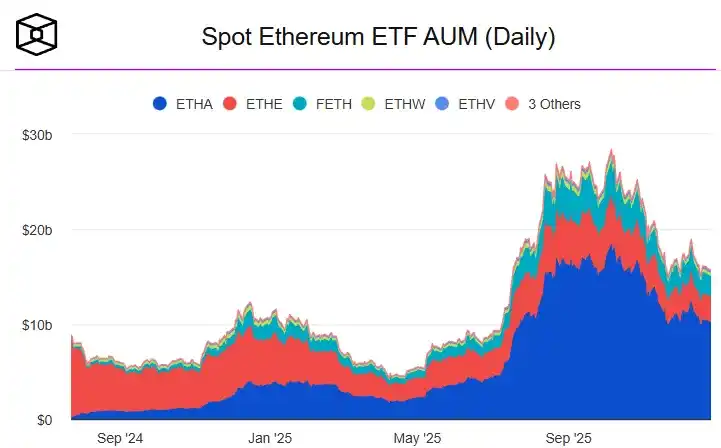

· Bitcoin and Ethereum spot ETFs go live.

· ETP framework achieves standardization (arguably paving the way for the DAT craze mentioned below).

· MiCA establishes a clear, unified regulatory approach.

· US passes Stablecoin Bill (GENIUS Act).

· Clarity Act one vote away from passage.

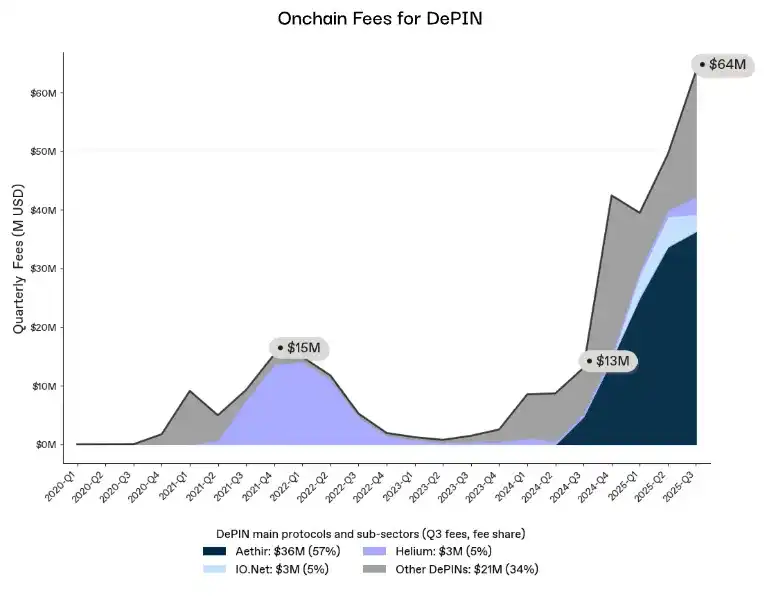

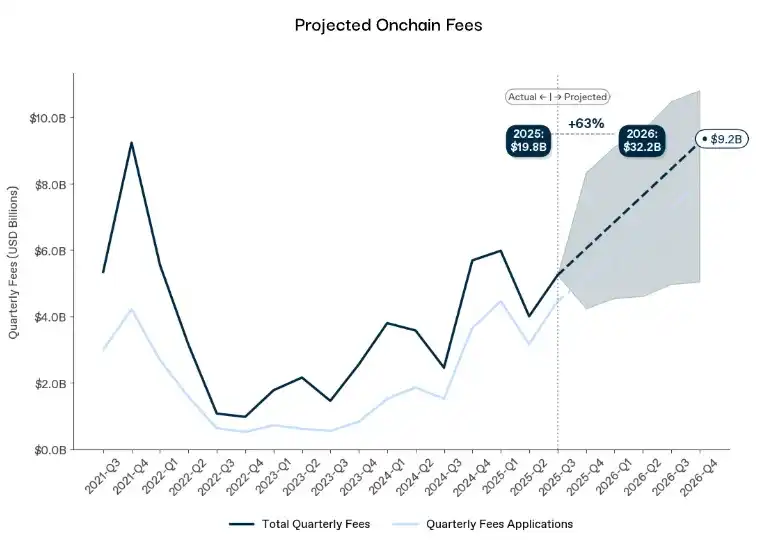

On-chain Fundamentals Hit All-Time Highs

Activity, demand, and economic relevance all see significant spikes:

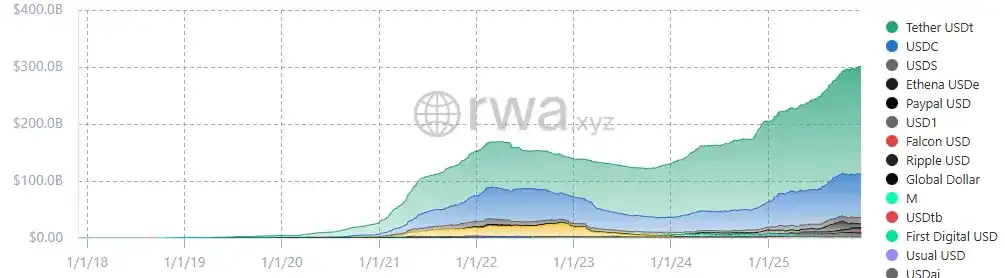

· Stablecoin supply surpasses $300 billion.

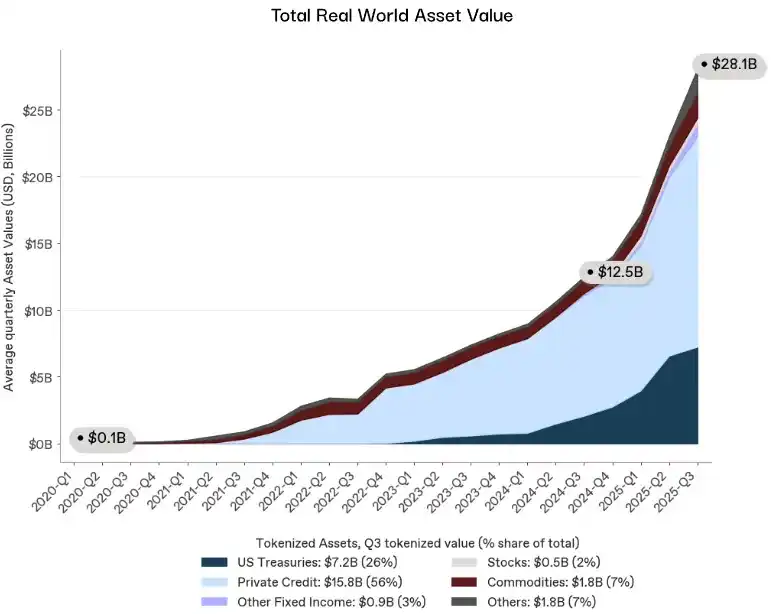

· RWA (Real World Assets) cross $28 billion.

· DeFi protocol income rebounds.

· On-chain fees march to new highs.

This is Clearly a Structural Issue

This is not a failure of demand, narrative, regulation, or macro conditions. It is a consequence of a fractured liquidity transmission system. The market structure that dominated 2017-2021 no longer exists, and no macro, regulatory, or fundamental force can resurrect it.

This does not mean the loss of opportunity, but rather a shift in how opportunity is generated and captured; over time, this shift will prove to be a decisive positive.

The previous market did indeed create a larger nominal “upside”, but it was structurally unsound. It rewarded reflexivity over fundamentals, rewarded leverage over utility, fostered manipulation, insider advantage, and extractive behavior, all of which are incompatible with institutional capital or mainstream adoption.

What went wrong?

Market liquidity is composed of three layers: capital providers, distribution channels, and leverage amplifiers. The collapse of Luna dealt a devastating blow to all three.

Liquidity Engine Stalls

From 2017 to 2021, the altseason was driven by a concentrated group of balance sheet providers willing to deploy capital across thousands of illiquid assets:

· Cross-platform market makers.

· Offshore lenders providing uncollateralized credit.

· Exchanges subsidizing the long tail.

· Prop trading firms hoarding risk.

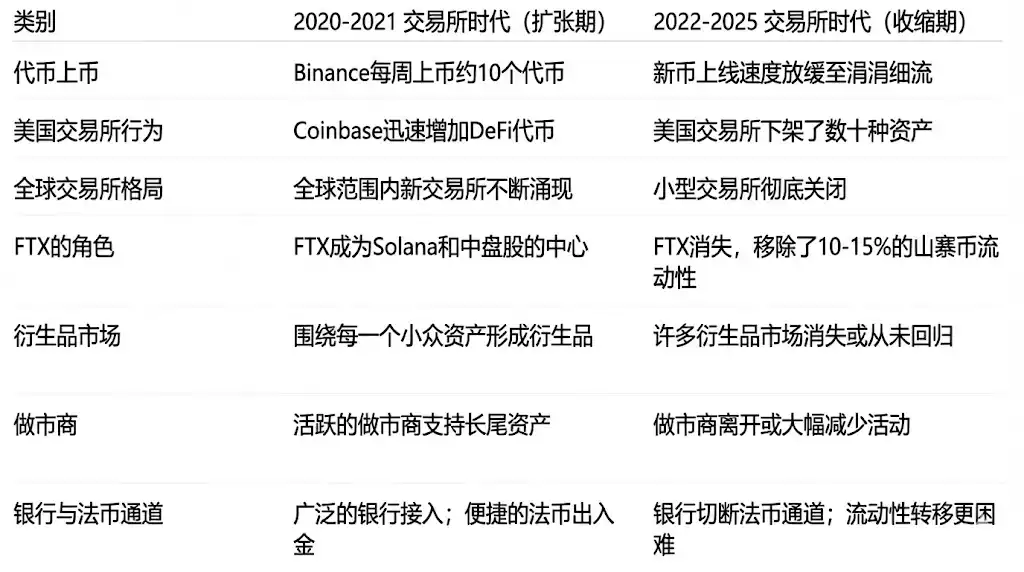

Then Luna collapsed. Three Arrows Capital (3AC) imploded. Alameda faced risk exposure. Genesis, BlockFi, Celsius, and Voyager went bust one after the other. Offshore market makers vanished. Capital providers disappeared, with no comparable balance sheet-sized, risk-tolerant, or willing entrants to long-tail markets.

Distribution Channel Breakdown

More critical than the capital itself is the mechanism to distribute the capital. Until 2022, liquidity naturally flowed down the risk curve as a handful of intermediaries kept shuttling it:

· Alameda smoothing prices across venues.

· Offshore market makers quoting thousands of pairs.

· FTX offering capital-efficient execution.

· Internal credit lines moving liquidity between assets.

As the Luna crisis spread to 3AC and FTX, this routing layer vanished. Capital could still enter crypto, but the pipes that once routed it to the long tail markets had ruptured.

Liquidity Amplifier Malfunction

Finally, liquidity was not only supplied and routed, it was also amplified. Small flows of liquidity could move markets because collateral was aggressively rehypothecated:

· Long-tail tokens being used as collateral.

· BTC and ETH being leveraged into a shitcoin basket.

· Recursive on-chain yield loop.

· Cross-platform rehypothecation.

Post-Luna, the system rapidly unraveled, with regulators freezing the remnants:

· SEC enforcement actions constrained institutional risk exposure.

· SAB-121 kept banks out of custody business.

· MiCA enforced stringent collateral rules.

· Institutional compliance departments constrained activity to BTC and ETH.

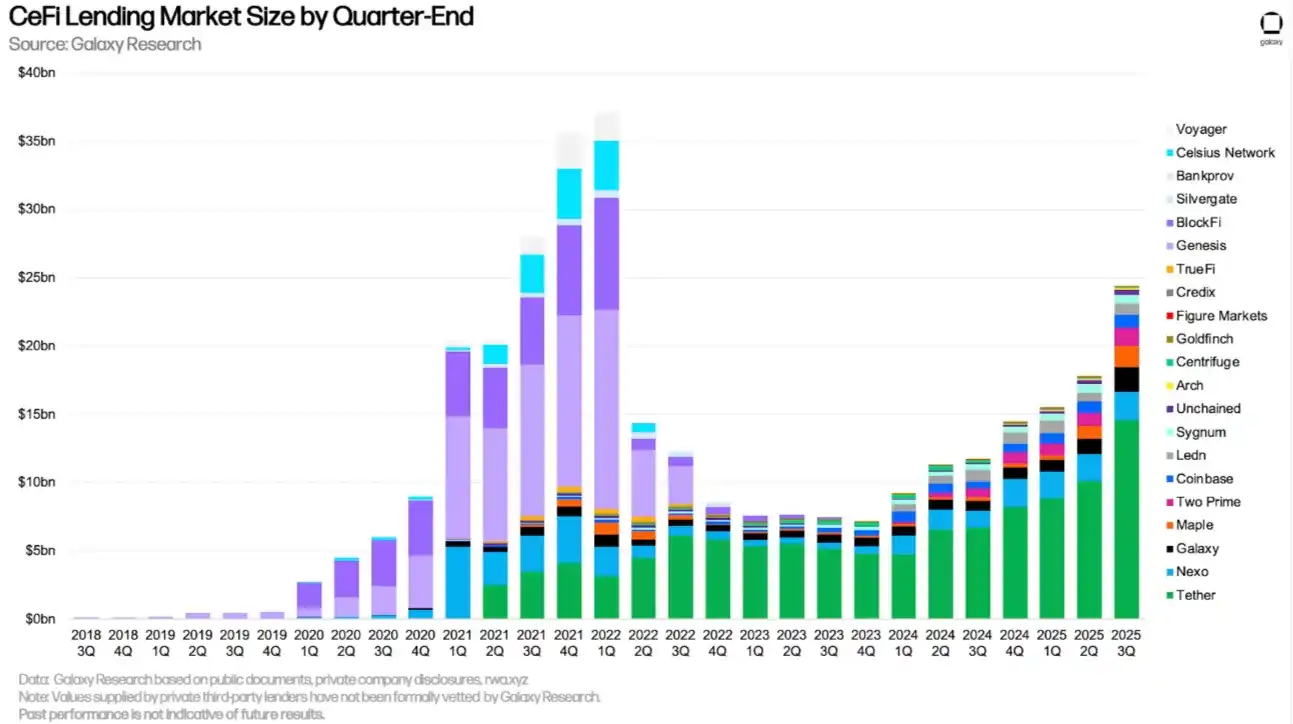

While the lending volume in CeFi's top tier has recovered, the underlying market has not. The lenders of the old regime, defined by credit transmission down the tail, have disappeared, replaced by a system more risk-averse and almost entirely concentrated on top assets. Resurfaced is lending without the long tail credit transmission mechanism.

This system could only operate when the leverage growth rate exceeded the risk exposure rate; a dynamic that foretold its ultimate failure.

Structural Shitcoin Liquidity Decay

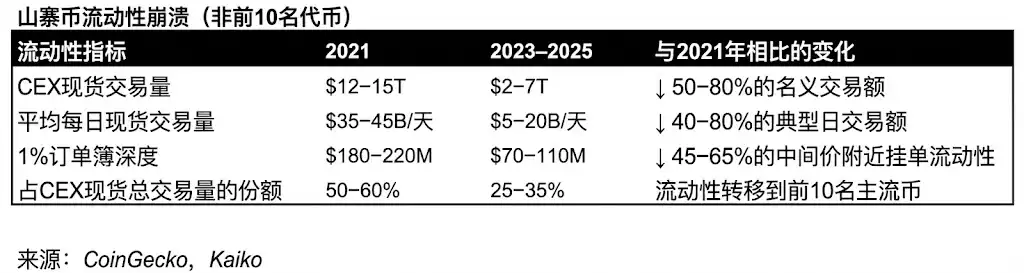

Once the engine stalled, the pipes broke, and the collateral amplifiers shut off, the market entered an unprecedented state: a prolonged structural liquidity decay lasting years. What followed was an entirely different market.

Market Depth Collapse

In history, the depth always recovered as the same cohort of players would rebuild it. But without them, shitcoin depth can never return to what it once was.

· Long-tail asset depth decreased by 50-70%.

· Spreads widened.

· Many order books have effectively been abandoned.

· Cross-exchange price smoothing mechanisms disappeared.

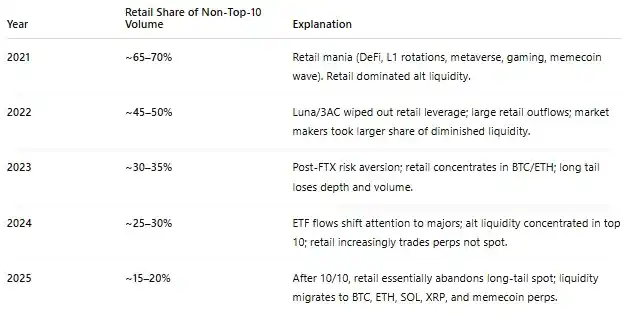

Demand Shifted to the Head

Liquidity migrated upstream with no downstream flowback.

· Institutional compliance departments prohibited tail exposure, sticking to mainstream assets like BTC and ETH.

· Retail exit.

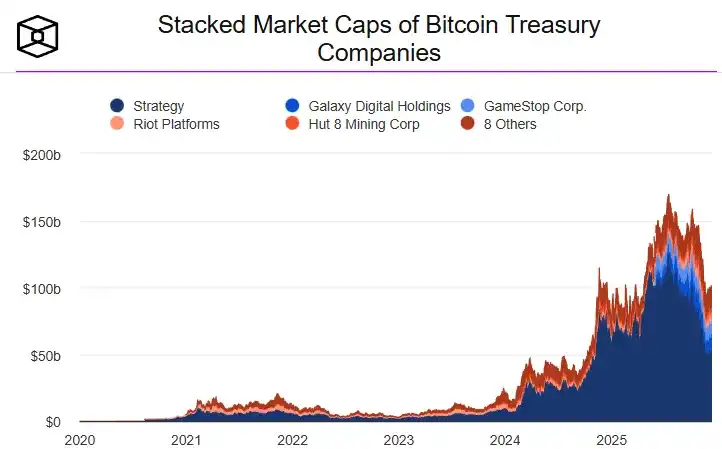

· ETFs and DATs focus exclusively on blue-chip tokens with sufficient existing liquidity.

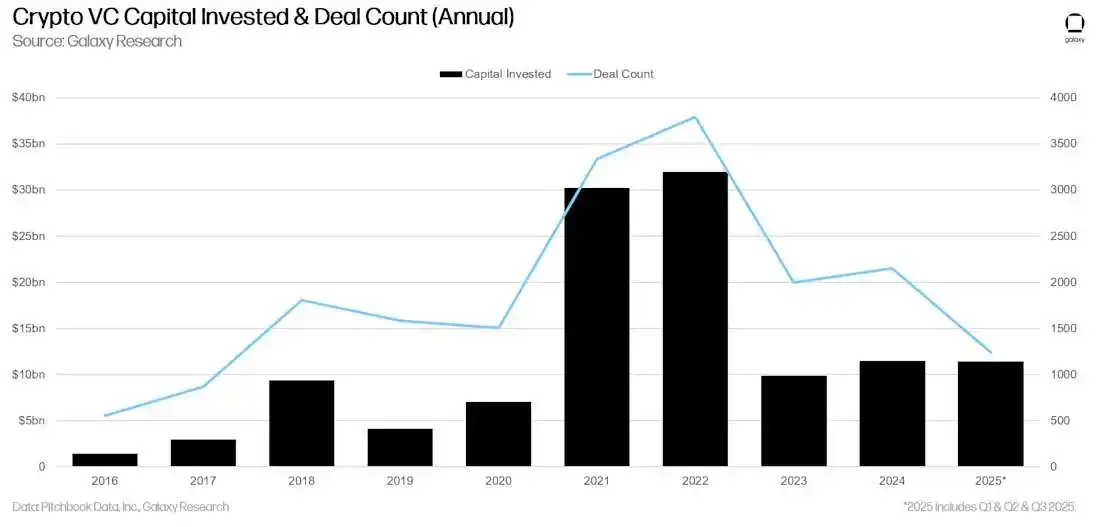

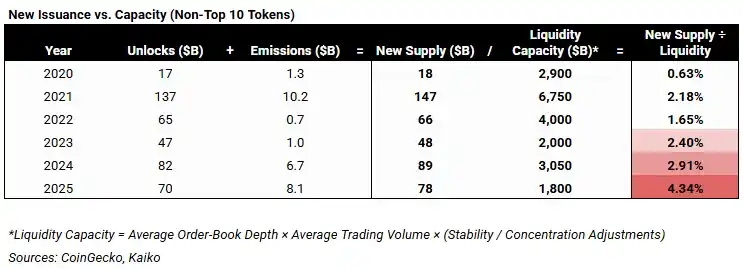

The Craze of Token Issuance Meets a Buyerless Market

The peak of VC activity in 2021/2022 has led to a massive future supply overhang.

As these projects issued tokens in 2024-2025, they encountered a market devoid of all absorption mechanisms. The damaged system couldn't withstand continuous selling pressure.

(With the clearing of the 2021-2022 VC issuance cycle, token unlocks are expected to normalize in 2026, alleviating a key structural barrier to long-tail liquidity)

The conditions that once fueled the alt season have been systematically dismantled. So, where do we find ourselves today?

Investing in the New Paradigm

Post-2022 has been painful for altcoins, but it represents a decisive break from a market structure fundamentally unsuitable for scaling. What follows is not a typical market pullback but a regime defined by reflexivity-lacking, leverage-driven liquidity. This absence continues to define the market to this day.

In the current structure, even assets with strong fundamentals trade under sustained illiquidity. Price action is dominated by a weak order book, limited credit, and fragmented routing, rather than fundamental performance. Many assets will stagnate long-term. Some will not survive. This is the inevitable cost of operating without artificial liquidity or balance sheet amplification.

This situation will only substantially change when regulation changes.

The imminent Clarity Act marks a pivotal inflection point in the altcoin market structure. It unlocks permission to enter a vast pool of capital: regulated asset managers, banks, and wealth platforms overseeing trillions of dollars, whose mandates prohibit them from holding risk exposure without clear legal classification, custody rules, and compliance certainty.

Until this capital can participate, the altcoin market will remain trapped in an illiquid regime. Once participation is possible, the market structure will undergo a profound transformation.

Major financial institutions are already positioning for this shift:

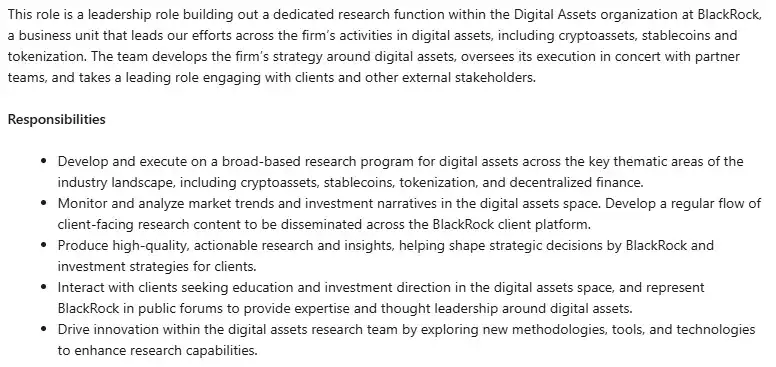

· BlackRock is establishing a dedicated digital asset research function to cover tokens akin to equities.

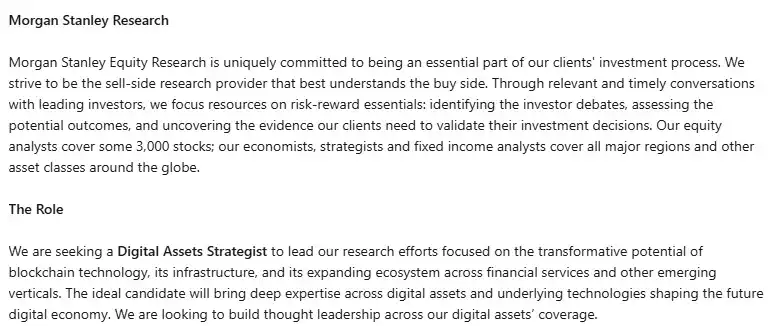

· Morgan Stanley is the same.

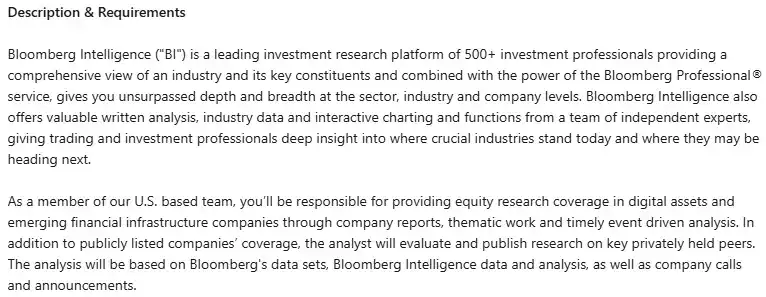

· Bloomberg as well.

· Cantor Fitzgerald has begun to release stock research-style reports on individual tokens.

This institutional build marks the beginning of a new market regime. Capital unlocked by regulatory clarity will not flow through offshore leverage, reflexivity loops, or retail momentum. It will trickle in slowly, selectively through familiar institutional channels. Allocation decisions will be driven by eligibility, longevity, and scale potential—not narrative velocity or leverage amplification.

The implications are clear: the old altcoin script is obsolete. Opportunities will no longer come from systemic liquidity tides. It will come from those able to weather sustained illiquidity through fundamentals, and prove institutional allocatability post compliance capital approval for specific assets.

Where once these filtering criteria were optional, in the new regime, they are mandatory.

· Sustained Demand: Does the asset capture recurring, non-custodial demand, or only see activity in incentives, narratives, or speculation?

· Institutional Eligibility: Can regulated capital hold, trade, and underwrite the asset without legal or custody risk? Regardless of technical merit, assets beyond institutional mandate will still be constrained by liquidity.

· Rigorous Economic Model: Supply, issuance, and unlocking must be predictable and constrained. Value capture must be explicit. Reflexive inflation is no longer tolerated.

· Proven Utility: Is the product being used because it offers a differentiated, valuable function, or is it relying on subsidies to survive while waiting for relevance?

In addition to stablecoins and tokenized assets (which continue to occupy mindshare), blockchain-based systems are also integrating into healthcare, digital marketing, and consumer-grade AI, quietly operating beneath the surface.

These applications are rarely reflected in token prices, and largely remain overlooked, not just by mainstream society, but even by many Web3 practitioners themselves. Their design is not for flashiness or viral spread; their appeal is subtle, embedded, and easily missed.

However, the shift from speculation to reality has begun: the infrastructure is live, applications are real, and novel differentiations have been validated. With more market participants turning toward institutional allocators and regulated capital, the growing adoption alongside the valuation gap will become increasingly hard to ignore.

Ultimately, this gap will close.

Stepping back, we've done it

I fell down the crypto rabbit hole for the first time in 2014, realizing then that blockchain was not just about digital currency but a disruptive technology for networks of data.

Ten years later, what once felt abstract is now operational in the real world.

Software can finally be both secure and useful: your data is controlled by you, kept private and protected, yet still leveraged to provide a genuinely better experience.

This is no longer experimental. It is becoming part of everyday infrastructure.

We have succeeded: not in achieving a "crypto supercycle," but in achieving the true objective.

It is now time for execution.

You may also like

What Happened in Crypto Today? Solana-Native Rails Launch on Digitap ($TAP) as the Best Crypto to Buy

Key Takeaways Digitap ($TAP) spearheads the transition toward real-world utility in cryptocurrency, offering a seamless financial ecosystem through…

Here’s Why Fed Contender Kevin Warsh is Seen as Bearish for Bitcoin

Key Takeaways Kevin Warsh is a potential nominee for the U.S. Federal Reserve chair, causing concerns due to…

XRP Price Breakdown Intensifies — Can Support Mitigate the Shock?

Key Takeaways XRP has dipped below the significant $1.80 mark, continuing its downtrend. The asset is trading beneath…

Kevin Warsh Associated with Crypto Project Basis and Electric Capital

Key Takeaways Kevin Warsh, former U.S. Federal Reserve Board Governor, is associated with crypto initiatives Basis and Electric…

Why is Trump’s Fed Chair Pick Kevin Warsh Seen as Bad News for Precious Metals, Commodities, Bitcoin, and Equities?

Key Takeaways: Kevin Warsh, once appointed, is expected to take a more hawkish stance on monetary policy, which…

Who Is Kevin Warsh? How His Fed Chair Odds Are Influencing Bitcoin Markets

Key Takeaways Kevin Warsh, a former Federal Reserve governor, is becoming a strong candidate for the next Fed…

Strategy (MSTR) Stock: Michael Saylor’s Bitcoin Bet Goes Red But Here’s The Twist

Key Takeaways Strategy’s Bitcoin investment has dipped below its average purchase price, highlighting market volatility. No immediate financial…

Bitcoin Hashrate Falls 12% After US Winter Storms Hit Miners

Key Takeaways: The total network hashrate for Bitcoin has declined by approximately 12% since November 11, marking the…

Gold’s Six-Month Rally Against Bitcoin Shows Parallels to 2019 Cycle

Key Takeaways Gold has consistently outperformed bitcoin over the last six months, despite being typically considered the haven…

Mantle’s Cross-Chain Era on Solana: Onboarding the Bybit Express to Mantle Super Portal

Key Takeaways Bybit joins forces with Mantle to enhance cross-chain asset flows through the Mantle Super Portal. Mantle…

XRP Price Outlook for 2026: Is Bitcoin Hyper Part of Long Term Themes?

Key Takeaways The potential future of XRP in 2026 is significant, with various factors influencing its growth and…

Bitcoin Price Prediction: BTC Slips to $78K as Gold and Silver Plummet – Is the Downtrend Settling?

Key Takeaways Bitcoin and traditional safe havens like gold and silver experience synchronized declines in a volatile market…

$30 Million Heist: Step Finance Treasury Wallets Breached

Key Takeaways Step Finance, a prominent Solana-based DeFi platform, faced a significant security breach, losing approximately $30 million…

Bitcoin Price Prediction: $50B Volume Drops 40% as BTC Tests $83K – Is a Breakdown Next?

Key Takeaways: Bitcoin’s trading volume has seen a significant decline, indicating cautious trader behavior. Bitcoin prices remain under…

Bitcoin’s 7% Drop to $77K Might Indicate Cycle Low, Analyst Suggests

Key Takeaways: Bitcoin has experienced a significant drop from $77,000 to around $78,600 after a modest rebound. Analyst…

Tom Lee–Linked Bitmine Faces Over $6B in Unrealized Losses on ETH Reserve

Key Takeaways: Bitmine Immersion Technologies reports significant unrealized losses exceeding $6 billion from its Ether reserves. The firm…

Silver Suffers Record 36% Drop as Precious Metals Crash – Is Bitcoin Primed for a Rally?

Key Takeaways Silver and gold undergo a historic collapse due to geopolitical and technical influences, culminating in significant…

XRP Price Prediction: $70M Liquidated as XRP Approaches $1.70 – Is $1.60 Next?

Key Takeaways XRP is experiencing a pronounced sell-off, struggling at the $1.70 level after a significant decline. A…

What Happened in Crypto Today? Solana-Native Rails Launch on Digitap ($TAP) as the Best Crypto to Buy

Key Takeaways Digitap ($TAP) spearheads the transition toward real-world utility in cryptocurrency, offering a seamless financial ecosystem through…

Here’s Why Fed Contender Kevin Warsh is Seen as Bearish for Bitcoin

Key Takeaways Kevin Warsh is a potential nominee for the U.S. Federal Reserve chair, causing concerns due to…

XRP Price Breakdown Intensifies — Can Support Mitigate the Shock?

Key Takeaways XRP has dipped below the significant $1.80 mark, continuing its downtrend. The asset is trading beneath…

Kevin Warsh Associated with Crypto Project Basis and Electric Capital

Key Takeaways Kevin Warsh, former U.S. Federal Reserve Board Governor, is associated with crypto initiatives Basis and Electric…

Why is Trump’s Fed Chair Pick Kevin Warsh Seen as Bad News for Precious Metals, Commodities, Bitcoin, and Equities?

Key Takeaways: Kevin Warsh, once appointed, is expected to take a more hawkish stance on monetary policy, which…

Who Is Kevin Warsh? How His Fed Chair Odds Are Influencing Bitcoin Markets

Key Takeaways Kevin Warsh, a former Federal Reserve governor, is becoming a strong candidate for the next Fed…